Tax brackets in the United States are a fundamental part of the progressive income tax system. Understanding how they work can help taxpayers maximize deductions, reduce liabilities, and ensure accurate tax filing. In this comprehensive guide, we will explore what tax brackets are, how they function, and how they impact your income.

What Are Tax Brackets?

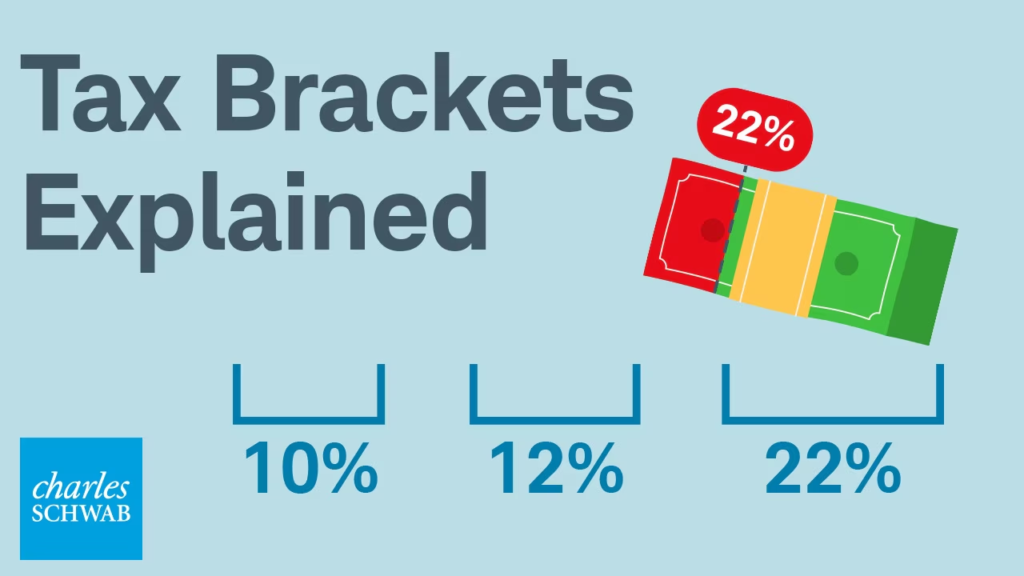

Tax brackets are income ranges that determine the rate at which an individual’s earnings are taxed. The U.S. has a progressive tax system, meaning that higher portions of income are taxed at higher rates. The Internal Revenue Service (IRS) sets different tax rates for different income levels, ensuring that lower-income earners pay a smaller percentage in taxes compared to higher-income earners.

Federal Income Tax Brackets

Each year, the IRS updates federal tax brackets to account for inflation. The U.S. tax system has seven tax brackets, with rates ranging from 10% to 37%. These brackets apply to different income levels based on filing status, such as single, married filing jointly, married filing separately, or head of household.

For example, in a given tax year, the brackets may look like this for a single filer:

- 10% on income up to $11,000

- 12% on income between $11,001 and $44,725

- 22% on income between $44,726 and $95,375

- 24% on income between $95,376 and $182,100

- 32% on income between $182,101 and $231,250

- 35% on income between $231,251 and $578,125

- 37% on income over $578,125

How Progressive Taxation Works

A common misconception is that earning a higher income moves an individual’s entire income into a higher tax bracket. In reality, only the portion of income that falls within a given bracket is taxed at that rate.

For example, if a single filer earns $50,000, the tax is calculated as follows:

- The first $11,000 is taxed at 10%.

- The income between $11,001 and $44,725 is taxed at 12%.

- The remaining income between $44,726 and $50,000 is taxed at 22%.

This progressive system ensures that individuals are not unfairly burdened by higher rates on their entire income.

State vs. Federal Tax Brackets

In addition to federal income taxes, most states impose their own income taxes, which may have flat or progressive tax structures. Some states, such as Texas, Florida, and Nevada, do not impose state income tax, whereas states like California and New York have higher progressive tax rates.

Impact of Tax Brackets on Deductions and Credits

Understanding tax brackets helps taxpayers optimize their tax returns by taking advantage of deductions and credits.

- Deductions lower taxable income, potentially keeping a taxpayer in a lower bracket. Common deductions include mortgage interest, student loan interest, and medical expenses.

- Credits reduce tax liability directly. The Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) can significantly lower the amount owed.

How to Reduce Tax Liability

There are several strategies to minimize tax liability and avoid moving into a higher bracket:

- Contributing to Retirement Accounts: Contributions to traditional IRAs or 401(k) plans lower taxable income.

- Utilizing Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): These accounts allow pre-tax contributions for medical expenses.

- Claiming Business Expenses: Self-employed individuals can deduct business-related expenses to lower taxable income.

- Timing Income and Deductions: Delaying bonuses or accelerating deductible expenses can optimize tax rates.

Changes to Tax Brackets Over Time

Tax brackets are adjusted annually for inflation, and they may also change based on new tax legislation. For example, the Tax Cuts and Jobs Act of 2017 significantly altered tax rates and bracket thresholds. Understanding these changes helps taxpayers plan ahead for future liabilities.

Conclusion

Tax brackets play a crucial role in determining how much individuals owe in federal income tax. The progressive system ensures fairness by applying higher rates only to higher portions of income. By understanding tax brackets, deductions, and credits, taxpayers can effectively manage their finances and reduce their tax burden. Planning ahead and utilizing tax-saving strategies can lead to significant financial benefits in the long run.