Inflation is an inevitable economic phenomenon that affects every individual, business, and government. It refers to the gradual rise in the prices of goods and services over time, reducing the purchasing power of money. When inflation rises, the same amount of money buys fewer goods and services, making everyday expenses more costly. Understanding inflation, its causes, and its effects on personal finance is crucial for safeguarding your wealth and ensuring long-term financial stability.

Understanding Inflation

Inflation occurs when demand for goods and services outpaces supply, leading to increased prices. It can be categorized into different types:

- Demand-Pull Inflation – Occurs when consumer demand exceeds supply, pushing prices higher.

- Cost-Push Inflation – Arises when production costs (wages, raw materials, transportation) increase, causing businesses to raise prices.

- Built-In Inflation – Develops when workers demand higher wages, leading to increased production costs and prices.

Governments and central banks, such as the Federal Reserve in the U.S., monitor inflation through indicators like the Consumer Price Index (CPI) and Producer Price Index (PPI). Moderate inflation is considered healthy for economic growth, but excessive inflation can erode purchasing power and create financial uncertainty.

How Inflation Affects Your Money

- Reduced Purchasing Power Inflation diminishes the value of money, making essential goods and services more expensive. As inflation rises, everyday expenses—such as groceries, fuel, and housing—consume a larger portion of your income.

- Savings Erosion Money saved in traditional bank accounts with low interest rates loses value over time if the inflation rate is higher than the interest earned. For instance, if inflation is 5% but your savings account yields only 1%, the real value of your savings declines.

- Higher Cost of Borrowing Inflation often leads to increased interest rates, making loans and mortgages more expensive. Higher interest rates impact credit card debts, student loans, and personal loans, increasing overall financial burdens.

- Investment Volatility Inflation affects different investment assets in unique ways. Stocks may benefit from inflation if companies can pass on costs to consumers, while bonds may suffer as higher inflation reduces their fixed interest value. Real estate prices often rise with inflation, making it an attractive hedge.

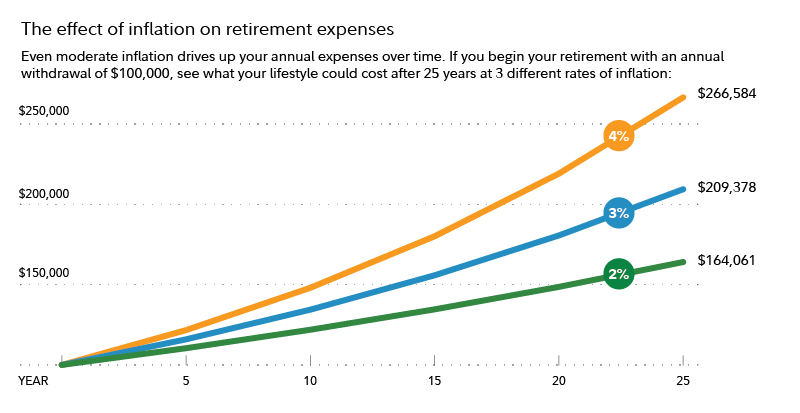

- Retirement Challenges Fixed-income retirees experience a decrease in their purchasing power when inflation erodes the value of pensions and Social Security benefits. Without proper financial planning, retirees may struggle to maintain their standard of living.

How to Protect Your Money from Inflation

To safeguard your finances from inflation, consider these strategic steps:

- Invest in Inflation-Protected Assets Treasury Inflation-Protected Securities (TIPS) are government-backed bonds that adjust their value based on inflation rates. These provide a reliable hedge against rising prices.

- Diversify Your Investments A well-balanced portfolio that includes stocks, real estate, commodities, and inflation-protected bonds can help mitigate inflation risks. Stocks historically outpace inflation over the long term, while real estate benefits from rising property values.

- Consider Precious Metals and Commodities Gold and silver have historically been used as a store of value during inflationary periods. Commodities such as oil, natural gas, and agricultural products tend to appreciate with inflation, offering a hedge against price increases.

- Increase Your Income Sources Relying on a single income stream can make you vulnerable to inflation. Explore side businesses, freelancing, and passive income sources such as dividend-paying stocks and rental properties to ensure financial security.

- Maintain an Emergency Fund Keeping an emergency fund in high-yield savings accounts or money market funds provides liquidity while offering some protection against inflation’s impact on daily expenses.

- Focus on Real Assets Investing in real estate, land, or tangible assets that appreciate over time helps maintain wealth in an inflationary economy. Rental properties generate passive income and can adjust rental rates to keep pace with inflation.

- Negotiate Higher Wages Inflation reduces the real value of salaries. Employees should consider negotiating wage increases or seeking job opportunities in industries with strong wage growth to maintain their purchasing power.

- Limit High-Interest Debt High-interest debts, such as credit cards and adjustable-rate loans, become more expensive with rising interest rates. Paying off debts early or refinancing with fixed-interest loans can help manage costs.

- Utilize Tax-Efficient Strategies Investing in tax-advantaged accounts, such as 401(k)s, IRAs, and Health Savings Accounts (HSAs), can help counteract the impact of inflation by maximizing after-tax returns.

- Monitor Inflation Trends Staying informed about inflation trends and economic policies helps make proactive financial decisions. Adjusting budgets and investments accordingly ensures preparedness for economic fluctuations.

Final Thoughts

Inflation is a powerful force that influences every aspect of personal finance. While it cannot be eliminated, understanding its impact and implementing proactive financial strategies can help protect your money and maintain purchasing power. By diversifying investments, seeking inflation-resistant assets, and making informed financial decisions, individuals can safeguard their wealth and secure their financial future against inflationary pressures.