Introduction

Understanding how taxes work can help you save money and make informed financial decisions. Two essential terms that taxpayers should be familiar with are tax credits and tax deductions. While both can reduce the amount of tax you owe, they work in different ways.

This guide explains the differences between tax credits and tax deductions, how they affect your tax return, and how you can use them to your advantage.

What Are Tax Credits?

A tax credit is a dollar-for-dollar reduction in the amount of tax you owe. If you qualify for a $2,000 tax credit, your total tax bill decreases by $2,000. Some tax credits are refundable, meaning you can receive a refund if the credit reduces your tax liability below zero. Others are non-refundable, which means they can only reduce your tax bill to zero but won’t result in a refund.

Types of Tax Credits

- Refundable Tax Credits

- Earned Income Tax Credit (EITC)

- Child Tax Credit (partially refundable)

- American Opportunity Credit (partially refundable)

- Non-Refundable Tax Credits

- Lifetime Learning Credit

- Child and Dependent Care Credit

- Residential Energy Credits

- Partially Refundable Credits

- The Child Tax Credit (up to $1,600 is refundable in 2023)

- The American Opportunity Credit (up to $1,000 is refundable)

How Tax Credits Work

Let’s say you owe $5,000 in federal taxes, and you qualify for a $2,500 tax credit. This reduces your total tax bill to $2,500. If the credit is refundable and your tax liability goes below zero, you might receive a refund.

What Are Tax Deductions?

A tax deduction reduces your taxable income, which in turn lowers the amount of tax you owe. Unlike tax credits, deductions do not provide a dollar-for-dollar reduction in taxes but instead decrease your taxable income based on your tax bracket.

For example, if you are in the 22% tax bracket and claim a $2,000 deduction, it reduces your taxable income, and you save 22% of $2,000, which is $440 in tax savings.

Types of Tax Deductions

- Standard Deduction vs. Itemized Deductions

- The IRS offers a standard deduction, which is a set amount that reduces your taxable income. In 2023, the standard deduction is:

- $13,850 for single filers

- $27,700 for married couples filing jointly

- Alternatively, you can itemize deductions, which include mortgage interest, medical expenses, and charitable donations.

- The IRS offers a standard deduction, which is a set amount that reduces your taxable income. In 2023, the standard deduction is:

- Common Tax Deductions

- Student Loan Interest Deduction – Up to $2,500 deducted from taxable income.

- Mortgage Interest Deduction – Interest paid on home loans can be deducted.

- Medical Expense Deduction – Only medical expenses exceeding 7.5% of your adjusted gross income (AGI) are deductible.

- Retirement Contributions Deduction – Contributions to traditional IRAs and 401(k)s reduce taxable income.

How Tax Deductions Work

If you earn $50,000 and qualify for a $5,000 deduction, your taxable income is reduced to $45,000. If you’re in the 22% tax bracket, this saves you $1,100 in taxes ($5,000 × 22%).

Key Differences Between Tax Credits and Tax Deductions

| Feature | Tax Credit | Tax Deduction |

|---|---|---|

| Effect on Taxes | Reduces the total tax owed dollar-for-dollar | Reduces taxable income |

| Value | More valuable because it directly lowers taxes | Less valuable, depends on tax bracket |

| Refundable? | Some are refundable | No, only lowers taxable income |

| Examples | Child Tax Credit, Earned Income Tax Credit | Mortgage Interest Deduction, Student Loan Interest Deduction |

Which Is Better: A Tax Credit or a Tax Deduction?

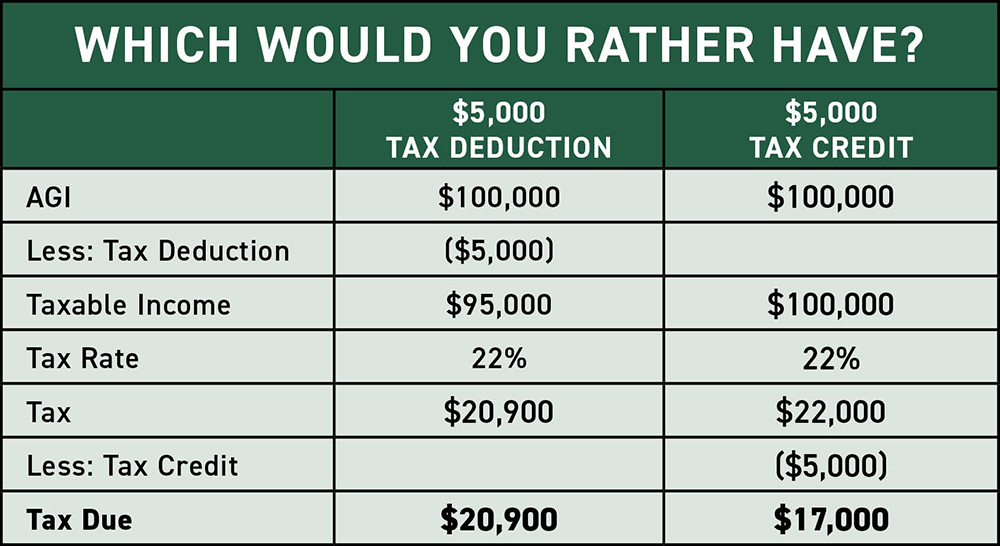

A tax credit is generally better than a tax deduction of the same amount because it directly reduces the taxes you owe, while a deduction only lowers your taxable income.

For example, if you’re in the 22% tax bracket:

- A $1,000 tax deduction reduces taxable income, saving you $220 in taxes.

- A $1,000 tax credit directly reduces your tax bill by $1,000.

Clearly, tax credits are more beneficial. However, tax deductions also play an important role in lowering your taxable income, especially if you qualify for multiple deductions.

Maximizing Tax Savings: Using Both Credits and Deductions

To minimize your tax bill, you should take advantage of both tax deductions and credits. Here’s how:

- Claim the Standard Deduction or Itemized Deductions – If your itemized deductions exceed the standard deduction, itemizing can save more money.

- Take Advantage of Tax Credits – Make sure you claim all eligible credits, especially refundable ones like the Earned Income Tax Credit (EITC).

- Contribute to Retirement Accounts – Contributions to a traditional IRA or 401(k) reduce taxable income.

- Use Education Credits – The American Opportunity Credit and Lifetime Learning Credit can help offset college expenses.

- Deduct Business Expenses – If you’re self-employed, deduct business expenses to lower your taxable income.

Common Tax Credit and Deduction Myths

Myth 1: Tax Deductions Give You a Dollar-for-Dollar Reduction in Taxes

Truth: Deductions lower taxable income, not the final tax bill. The actual tax savings depend on your tax bracket.

Myth 2: You Can Claim Both the Standard Deduction and Itemized Deductions

Truth: You must choose either the standard deduction or itemized deductions, not both.

Myth 3: Higher Income Earners Don’t Qualify for Tax Credits

Truth: Some credits, like the Earned Income Tax Credit, have income limits, but others, like education credits, may still be available for higher-income taxpayers.

Conclusion

Tax credits and tax deductions both help reduce your tax bill, but they function differently. Tax credits provide a direct reduction in the amount you owe, making them more valuable than deductions, which only reduce taxable income. However, by using both deductions and credits, you can significantly lower your tax liability and maximize your tax refund.

When preparing your tax return, always look for available credits and deductions to ensure you’re paying the least amount of taxes legally possible. If you’re unsure which tax benefits you qualify for, consulting a tax professional or using tax software can help you optimize your return.

Would you like me to expand on any section or add more details?